A new year has begun, and the facts and figures of 2022 has been disposed of in one of the folders on the bookshelf (I’m one of these people who like things physical). What a year it was – the underlying thesis of Climate Change starting to hurt portfolio performance got off to a pretty flying start, and there will be a lot more where that came from…even if a best case scenario plays out from here.

My own performance was satisfactory, helped by getting the macro back-drop right, some hard work, not least from the two youngsters who assisted me through the rough and smooth by going through lots of research and crunching numbers, as they kept questioning my views of the world, and last but not least, a very disciplined approach during difficult moments. Not surprisingly, the free and unconstrained portfolio delivered the highest return, helped by shorts in both stocks and bonds, some fabulous option strategies on Gold, a bullish dollar view early in the year and some pretty aggressive positioning for high inflation prints in the USA, UK, Sweden and Canada through linkers. The long-only book’s performance was far more modest (5.5%), as was volatility (4.5%), and neither was helped by an ugly 4% drawdown in October when I completely misread the market. Fixed income was, not surprisingly, a complete absentee, but the cash position was pretty large and varied between 20% (beginning of the year) and 55% (end of June), becoming an increasingly useful ally as rates kept rising through the year. Despite missing out on the q4 rally, I never felt bonds at any point during the course of the year warranted a buy – and I still think they look deeply unattractive, and credit, if possible, even more so. The stock selection was quite concentrated and never exceeded more than 18 names, averaging about 12, as I deployed a lot of tactical sector rotation around a core-long of 8-9 names. Large caps were much preferred to mid- and small caps.

Leaving yesterday’s news on the bookshelf, where it belongs, and looking ahead to the end of the Fed-meeting tonight, it doesn’t strike me as a potentially huge market-mover. Perhaps because of that more caution than usual might be warranted, but given that the Jezza-led FOMC once again seem to have succumbed to market-bullying, leaving them no option but to hike by the fully priced quarter, it’s hard too see how the market will react violently to the announcement. Maybe the statement will result in a bit more commotion, but then again, it’s equally hard to see how the Fed will only do 25 and then try to back-stab the market with an overly hawkish statement. The truth is that this FOMC simply haven’t got those kind cojones.

Where does that leave the market ? Not in a good place for sure. Bonds remain virtually uninvestible at these yield levels, and credit in all its guises is still equally unpalatable, while equities, except for a few token EM’s, look positively incomprehensibly priced. Don’t get me wrong – there are still names out there worth buying, preferably in the sell-offs, of companies that produce genuinely needed goods and services, but there aren’t many of them. They are typically battle-hardened businesses with positive cashflows that don’t rely on aggressive operating and financial leverage to hit unrealistic growth targets, or, like David and I like to call it, climate leverage. Buy those names when the market allows you to, because others will, as they will be the survivors in tomorrow’s increasingly hostile world. Keep selling beta and, if you have the ability to go short, those companies that rely heavily on climate leverage in their “business-models”.

What about January, and the extended Santa-rally ? That, in my opinion, is truly the gift that keeps giving. I have happily chipped out some beta, and taken partial profit in some runaway names through this January-pop, and will equally happily keep doing so in the unlikely event it extends into a February-pop. Why ? Because hope is not a viable investment strategy. This is still a bear market, and bear markets simply don’t end against a macro back-drop like this, and at valuations like these.

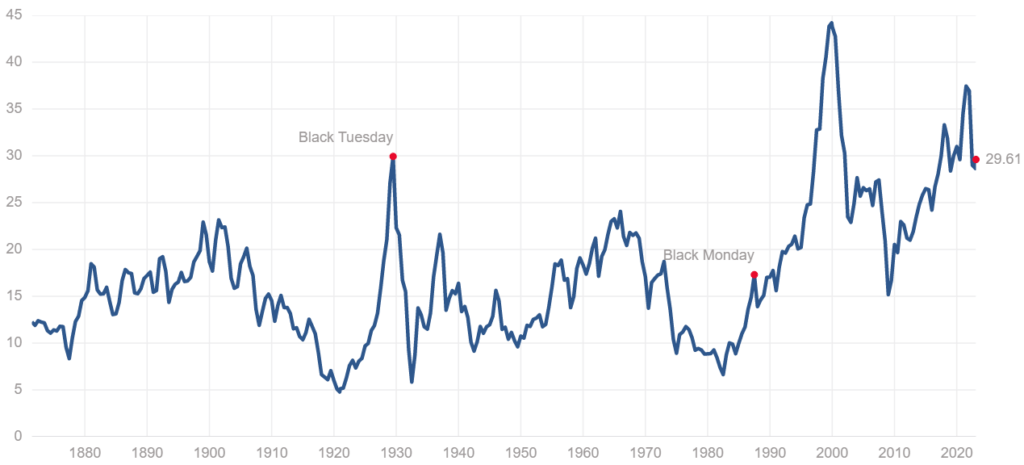

With a Shiller P/E of almost 30, it’s worth reminding people that the valuation of S&P500 at the current level is virtually the same as when the market peaked in October 1929. Incidentally, so is the yield of the 10-year Treasury Bond, while inflation is actually several percent higher. For those of you who think the Shiller measure has lost its potency, predictive power, and ability to correctly value the market, it’s worth pointing out that its earnings were priced at 18 times then – vs 22 now.

The macro picture is an even bigger hindrance to a further advance. While economic data is holding up ok in some respects, it’s getting harder and harder to paper over the cracks. Retail sales globally is collapsing in all kind of places (Australia, Germany, Sweden etc), while strikes are now commonplace in many countries, and on a scale not seen for decades. Climate Change might only just have started to bite, but the disruptions it causes are manifesting themselves everywhere – container ships being lost in storms, floods stopping the flow of goods, and with increasing frequency, as well as intensity, droughts affecting crop yields etc. At the same time as there are labour shortages in some sectors, lay-off announcements keep hitting the wires at an ever-increasing rate, and it’s no longer confined to just the tech-sector. While all this is taking place, the lagged effects of previous monetary tightening is now starting to deliver pain to cash-starved businesses who for years have had faith in a growth-centred, “build it and they will come” model, and it’s most definitely worth remembering that all this is happening while S&P500 profits are actually falling year-on-year.

The structural headwinds for a bull market have not gone away in the last year and, if anything, they have intensified. Global financial leverage, and by extension indebtedness, has reached a new all-time-high, and the peace dividend that Generation X (that’s me) have kept harvesting for decades has been cut – permanently. The world is far more unstable geopolitically than it’s been for a long time, and that means globalisation is now in full retreat, and investors everywhere should really consider the following. Is it realistic to expect 30 years of increased global operating leverage to be unwound in 12 months ? If you answer that question with a ‘yes’, I really wish you the very best of luck going forward. Because you are going to need it.

All this makes it basically irrelevant whatever Powell & co decide to do later today, because their ability to influence the market short- and medium-term is truly very limited. A far better use of time and effort is to focus on the road ahead, because it’s long and winding, and keep enjoying the gift from the old fellow with the white beard – the one that keeps giving.

{kind=link}